From Wikipedia, the free encyclopedia

Type of official watchdog institution

A

fiscal council

is an independent body set up by a government to evaluate its

expenditure

and

tax policy

. Typically, councils are staffed by

economists

and

statisticians

who do not have the ability to set policy, but provide advice to governments and the public on the economic effects of

government budgets

and

policy

proposals. Some fiscal councils also provide

economic forecasting

. Fiscal councils evaluate government's

fiscal policies

, plans and performance publicly and independently, against

macroeconomic

objectives related to the long-term sustainability of public finances, short-to-medium-term macroeconomic stability, and other official objectives.

[1]

History

[

edit

]

Several fiscal councils arose following the

financial crisis of 2007?08

with the intention of avoiding

debt crises

and alleviating the problem of

deficit bias

, which is a tendency of governments to allow increasing long-term deficits.

[2]

Analysis from the

International Monetary Fund

proposes that deficit bias results from both voters and

policy-makers

? the former through imperfect information on budgets and neglect for future generations, and the latter through

imperfect information

,

information asymmetries

, electoral pressures, a

common-pool problem

among government agencies, and a combination over optimistic spending and growth projections.

[3]

Fiscal councils alleviate deficit bias by providing independent

non-partisan

estimates of government income, and by reminding the public of the government's

intertemporal

budget constraint.

[3]

The public will then, in theory, react to this information by supporting governments that deliver sustainable fiscal policies and electorally punishing governments that are fiscally irresponsible.

Fiscal councils, such as the United Kingdom's

Office for Budget Responsibility

, have been criticised for mostly advising from the perspective of

neoclassical economics

and advocating for balanced-budgets and

small government

, to the detriment of

heterodox economic

approaches based on the

real economy

and more interventionist

New Keynesian

approaches to the

business cycle

.

[4]

[5]

[6]

Deficit bias

[

edit

]

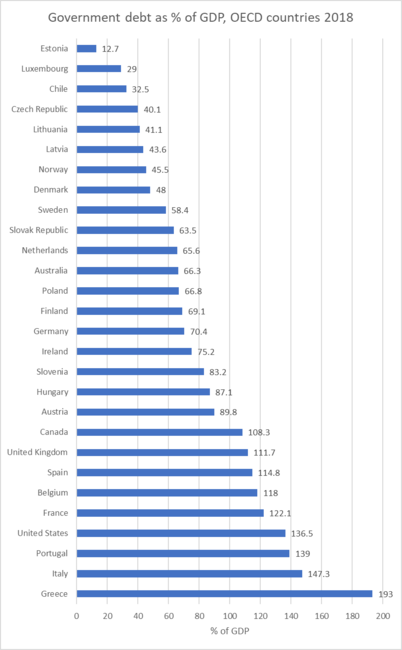

Government debt as % of GDP, OECD countries 2018

Government debt as % of GDP, OECD countries 2018

More countries in the world run budget deficits than not.

[7]

In the long term, a high budget deficit is unsustainable. High budget deficits have aggravated crises like the

European debt crisis

. Governments that are unsure of being re-elected may ignore the long-term consequences of fiscal deficits and use generous fiscal policy to increase their chances of re-election. Voters may favour fiscal deficits because they benefit from tax cuts and public spending increases, and only bear part of the cost, the rest being borne by future generations. Alternatively, electorates vote for deficits because they are not fully aware of the problem.

[8]

List of fiscal councils

[

edit

]

References

[

edit

]

- ^

Calmfors, Lars; Wren-Lewis, Simon (2011-04-21).

"What are fiscal councils, and what do they do?"

.

VoxEU.org

. Retrieved

2019-11-28

.

- ^

Weldon, Duncan

(2016-07-26).

Whatever happened to deficit bias?

. Bull Market. Retrieved 2020-03-14.

- ^

a

b

IMF (2013).

"The functions and impact of fiscal councils"

(PDF)

.

- ^

Labour and the politics of budget responsibility

. SPERI (2013-10-15). Retrieved 2020-03-14.

- ^

Skidelsky, Robert (2018).

Money and Government: The Past and Future of Economics

. Yale University Press. pp. 230?233.

ISBN

9780300240320

.

- ^

Mostacci, Edmondo (2016).

From the Ideological Neutrality to the Neoclassical Inspiration: The Evolution of the Italian Constitutional Law of Public Debt and Deficit

.

University of Genoa

.

- ^

"The World Factbook ? Central Intelligence Agency"

.

www.cia.gov

. Archived from

the original

on December 10, 2011

. Retrieved

2019-11-28

.

- ^

Krogstrup, Signe; Wyplosz, Charles (2009), Ayuso-i-Casals, Joaquim; Deroose, Servaas; Flores, Elena; Moulin, Laurent (eds.), "Dealing with the Deficit Bias: Principles and Policies",

Policy Instruments for Sound Fiscal Policies: Fiscal Rules and Institutions

, Finance and Capital Markets Series, Palgrave Macmillan UK, p. 5,

doi

:

10.1057/9780230271791_2

,

ISBN

978-0-230-27179-1